Public markets once captured the majority of value creation for high-growth tech companies. Today, that value is increasingly created in the private markets, leaving public investors on the sidelines as private companies hit trillion-dollar valuations. Twenty years ago, the conventional wisdom was simple: invest early in a company like Amazon or Google, hold for decades, and compound at seemingly endless rates, all in the public markets.

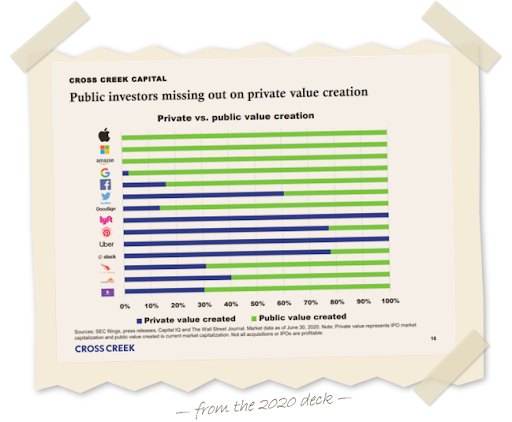

Starting in 2015, this narrative began to change. Private companies began to raise $100M rounds, a scale of capital previously associated with traditional small-cap IPOs. Internally at Cross Creek, we started calling these "private IPOs." Late-stage crossover investors and even public market players began participating in these financings, a clear sign that the lines between private and public capital were blurring. It was an early signal that the private markets were steadily absorbing value creation that had long belonged to public investors. We shared the following slide in our 2020 annual meeting to highlight this trend:

The shift has now reached mega-cap scale. OpenAI's $122B private financing at an $852B valuation is the largest private raise in history, dwarfing traditional public offerings. SpaceX, now merged with xAI at a $1.25T combined valuation, tells the same story: when it eventually lists, it will immediately rank among the largest public companies in the world, yet public market investors will have sat out the entire era of value creation.

As investors in the private markets, we've wondered if the ecosystem has overextended itself in enabling mega-cap companies to stay private longer. While there are clear benefits, such as the ability to focus on long-term results and more control of cap tables, there are meaningful externalities as well. One is the risk that public markets may not support the private valuations. In the private markets, it's possible to hide behind valuations, as information is not widely available and price discovery is infrequent. Public companies, in contrast, are continuously valued and quickly revalued when fundamentals and narratives change.

This dynamic has broader implications. Public indices are becoming less representative of the innovation economy, as many of the most important companies remain private through their highest growth phases. This may compress returns for the public markets, especially given that many of the largest contributors to index gains (e.g., Nvidia, Alphabet, Microsoft, Amazon, and Meta) are venture-backed tech companies.

This trend may begin to reverse if companies start to view the public markets as an attractive alternative to private capital, but today it's clear that the public markets have missed out on the opportunity to invest in many of the next generation of high-growth platform companies, such as Anthropic, OpenAI, Stripe, Databricks, and SpaceX, which are poised to transform the economy.

The real question is what role public markets will play when these companies arrive: validator or disciplinarian?

This material does not constitute an offer to sell or the solicitation of an offer to buy any securities. Securities of any fund are offered to selected investors only by means of a complete offering memorandum and related subscription materials which contain significant additional information about the terms of such an investment. The foregoing consists solely of recent news relating to certain Portfolio Companies. These Portfolio Companies do not represent all of the investments made or recommended by Cross Creek. The reader should not assume that an investment in any Portfolio Company identified was or will be profitable. Past performance is not indicative of future results. Investors should be aware that a loss of investment is possible. The research for this material is based on current public information that we consider reliable, but we do not represent that the information herein is accurate or complete, and it should not be relied on as such. Our views and opinions expressed herein are current as of the date this material is sent and are subject to change without notice. Not all acquisitions or IPOs are profitable; the positions can be acquired at a price that is greater or less than the price at which Cross Creek purchases its interests for client accounts. A link to Cross Creek's direct company holdings is available on our website.